Paying down debt can go such a long way to living a better, healthier life. Less debt means less stress, but it also means less time spent having to find ways to make sure the bills are paid each month.

In January 2016, our household debt totaled over $200,000.

Now you might think that someone with nearly $200,000 of debt must have a serious spending problem. That or a very nice house, a fancy car, perhaps an addiction to the smell of burning money… SOMETHING, right?

Nope.

How to Pay Down Debt Fast

All we have to show for our debt is an 8 year old mini-van, a 130 year old fixer-upper of a home, and two college degrees that between us cost $150,000.

The Debt Breakdown

Full disclosure, here is our debt breakdown from January 2016:

- Lowes Credit Card: $2,800

- Furniture Row Credit Card: $1,782

- Private student loans: $96,646.09

- House: $43,600

- Car: $17,970.23

- Federal Student Loans: $46,094.17

Grand total: $208,892.49

Living Paycheck to Paycheck

Our Lowes and Furniture Row bills are (were) the only credit card debt we had. We used both when we purchased our house in August of 2014 so that we could purchase some much needed appliances and furniture. Fortunately they both offered zero percent interest for a set amount of time, but still – $4,600 in credit card debt is a huge chunk of change to carry around.

Meanwhile, my husband and I both have a LOT of student loan debt. Despite both of us working while in college, we fell into the trap of taking out way more than we should have.

Rather than taking the smarter route and going to a community college first, I spent all four years at a private school that cost me about $36,000/year. My partner did go to a community college first, but was still persuaded to take out a lot of student loans to help support himself while in school.

Nearly $150,000 in student loan debt and together our jobs net us $33,000/year (after daycare is factored out…)

So how in the world have we managed to pay down over $10,000 in debt in two months?

Well, our first step was to take a look at our budget and figure out where the majority of our money was going. We were paying $1,600/month towards our debt but the overall total was only decreasing by $1,100. Once we figured out why and how that was happening, we were able to change things up to make a more significant dent in our debt.

Disclaimer: This post does contain some affiliate links, which means I may earn a small commission should you click through. This is no way impacts my recommendation of any products or services.

Does the Snowball Method Work?

Some financial gurus recommend you snowball your money (pay off the smallest debts first, get a “high” from paying off a bill entirely, then roll that payment towards paying off the next smallest debt).

Here’s my problem with that:

Let’s say you owe one credit card $2,000 with 0% interest for three years (such was the case with my Furniture Row card) and another credit card is owed $4,000 with 24.9% interest (the usual rate for most Lowes purchases).

You have $300 to put towards your debt each month. If you put $170 towards the first debt and only $130 towards the second, it will take you a year to pay off that first card.

Meanwhile, in that year, you’ve put $1,560 towards that second card but have only paid it down by about $500 – that’s not even a third!!

So with the snowball method, you’ve put $3,600 towards your debt but at the end of one year, you will still owe over $3,500 (that will now take you another 14 months to pay off and cost you an additional $700 dollars).

Snowball method: Pay $300 for 26 months, $6,000 of debt = $7,800

Pay Debt Based on Interest Rates

So what if you reversed it and paid the minimum due on the zero interest and the rest towards the second card?

You’d be looking at $70 towards the first card, $230 towards the second.

In the first year, you would put $2,760 towards your second card, $2,070 of which would be towards the principal.

In the end, paying based on interest rates, you would be free of these two debts in less than two years.

Paying based on interest rates: Pay $300 for 24 months, $6,000 of debt = $7,200

So not only would you save yourself nearly $600, but you’d also have an additional $300/month two months sooner than you would with the snowball method.

That’s $1,200 you can now throw towards another debt (like your mortgage!)

Snowballing Debt

Now I will say that the snowball method has been proven to work for many people and it can be an effective way to motivate yourself to pay down those debts. But depending on your financial situation, you might be paying quite a high price for that motivation.

So for today, the first thing to do to get started towards paying down $10k like I did is to look at your budget and list out every debt you owe, the APR on it, and what you’re currently paying each month. Don’t have a budget? Read this quick and easy post to develop a budget TODAY!

Having a good grasp on your financial situation is the very first step to improving it.

Maximize Your Tax Return

When the new year begins, people are often really struggling with debt. You want to set a resolution to become debt free but you’re coming off of the holiday season with bags of presents that translate into slips of paper covered in financial regret.

It’s easy to see why you might look to tax return time with a glimmer of hope.

The problem, however, is that more often than not, tax returns are seen as a way to buy new stuff; the cheapest time to buy cars, for instance, is right before tax season, as dealers want to get rid of old stock and they know people are about to have pockets full of “discretionary” money.

I know a lot of people who get their tax returns and buy handbags, TVs, go gambling, buy an ostrich, or whatever other things suddenly become a “need” in their eyes. Now I’m not here to judge, I’m just sayin’…

Stop Seeing It As “Free Money”

That money isn’t just given to you by the government! It is money that you earned, one way or another, that the government was holding until your tax variable whosits decided you didn’t owe them anything.

If the government wasn’t taxing that money out of your check, would you just drop 15% of your paycheck each month on carnival games and gumballs?

For the 99.9% of us who aren’t Willy Wonka — of course you wouldn’t! Please stop thinking of it as free money and start realizing it should be allocated towards paying down your debt.

There’s no doubt that there’s a psychological high to getting a big windfall dumped in your lap, but if you truly have a good grasp on your financial situation, you know that “windfall” could translate into so much more.

By allocating my $5,500 tax refund towards my debt, I saved myself nearly $1,300 that I would have otherwise paid out in interest over the next year.

Was it tempting to spend that money on a vacation or some nifty new cleaning supplies? Yes absolutely. I totally believe in treating yourself once in a while, but I also know it’s better to front load your life and pay down debt now versus having it stick to you for decades.

How to Make the Most of Your Tax Return

If you’ve already received your tax refund, I want you to take a genuinely honest look at how you allocated that money. Did you spend it wisely? Or did you spend it in a way that’s going to cost you so much more in the long run? How can you do better next year?

Seriously make note of this and then I want you to hop over to FutureMe – a website in which you can write an e-mail and schedule it to be sent to your future self. Write a quick e-mail and motivate your future self to do better next year. Schedule it to be sent on January 2nd of next year so you don’t forget to do better!

If you haven’t yet received your tax refund, I want you to open up your list on debts and figure out how you can best allocate that money. Is there a bill you can pay off entirely? Or would it be better to divvy it up among a few of them? Figure out a plan and FOLLOW THROUGH with it! Budget your estimated tax return towards your debts, not towards a trip or new frivolous purchase.

Evaluate Your Tax Situation

And for those of you who don’t get returns (or worse – have to pay!) now is a good time to re-evaluate that situation. Chances are good that you have less being taken out in taxes with each paycheck than the rest of us. That’s great provided you’re spending it wisely. But if you don’t yet have a strong hold on your financial situation, then maybe you should talk to your employer about changing up your W-4. While I don’t necessarily advocate asking the government to save your money for you – there are ways to trick yourself into saving otherwise – it’s not a bad thing if you then allocate your return towards debt.

Develop Additional Income Streams

Or rather, that should say: “Develop Additional Income Streams And ONLY Use The Money To Pay Off Debt” but that’s a bit of a mouth…err…eye-full?

Anyway, as it sounds, developing additional income streams is key to getting your debt paid down faster, which I’ve already talked about, but it bears repeating.

I hope by now you’ve developed your own budget and I hope you’ve done so based only on your primary income. Please don’t ever use possible or imaginary money when it comes to planning out your financial future!

With that said, including only your primary income in your budget means that any extra money that comes your way can (and should) go directly towards your debt.

Consider this: for most people, one extra mortgage payment per year will pay their house off seven years sooner. That’s one extra payment for seven years of debt freedom. What are those seven years worth to you?

There are a lot of ways to earn some extra money (that don’t involve the removal of clothing or the selling of body parts). A part time job, though not necessarily glamorous, will generate reliable extra income that you can have direct deposited into an account that automatically makes a payment to a bill each month. It’s a great way to not even be tempted to spend that extra money.

Don’t have the time to work an additional job outside the home? That’s okay, neither did I!

My Favorite Ways to Make Extra Cash

If you can write, Textbroker.com should be your go-to site to generate extra money quickly and easily. You provide a short writing sample, they evaluate it and rate it 1-5 stars, and you earn money based on your star rating. I’m at 4 stars and I earn about 1.4 cents/word. It doesn’t seem like much, but if you enjoy writing and can do so quickly, it adds up fast. I’ve made close to $800 since the beginning of the year. That’s a tremendous amount of money for something I do over my lunch hour a couple days a week.

Do you like to talk instead of write? UserTesting.com has recently become one of my favorite ways to earn extra income. I keep the site open whenever I’m online and if I hear the “ping” telling me a job is available, I jump on it! 15 minutes later and I’m $10 richer!

Upwork.com is another site where you can apply for freelance jobs online. Writing, design, coding, virtual assistant work – all of these and so much more! You can pick up a variety of jobs fairly easily, with little hassle plus you are in charge of the price. The better you are, the higher you can charge, and there’s thousands of offers on the site all the time. I’ve made $150 from them so far this year and the majority of that is actually from companies approaching ME. It’s great!

Lastly, check out InboxDollars! And be sure to read on how to make the most money on InboxDollars.

As I mentioned, I’ve gone over a few of these and then some in another post, but these are a few of my favorites. Just from working from home, I’ve managed to make nearly $3,000 this year.

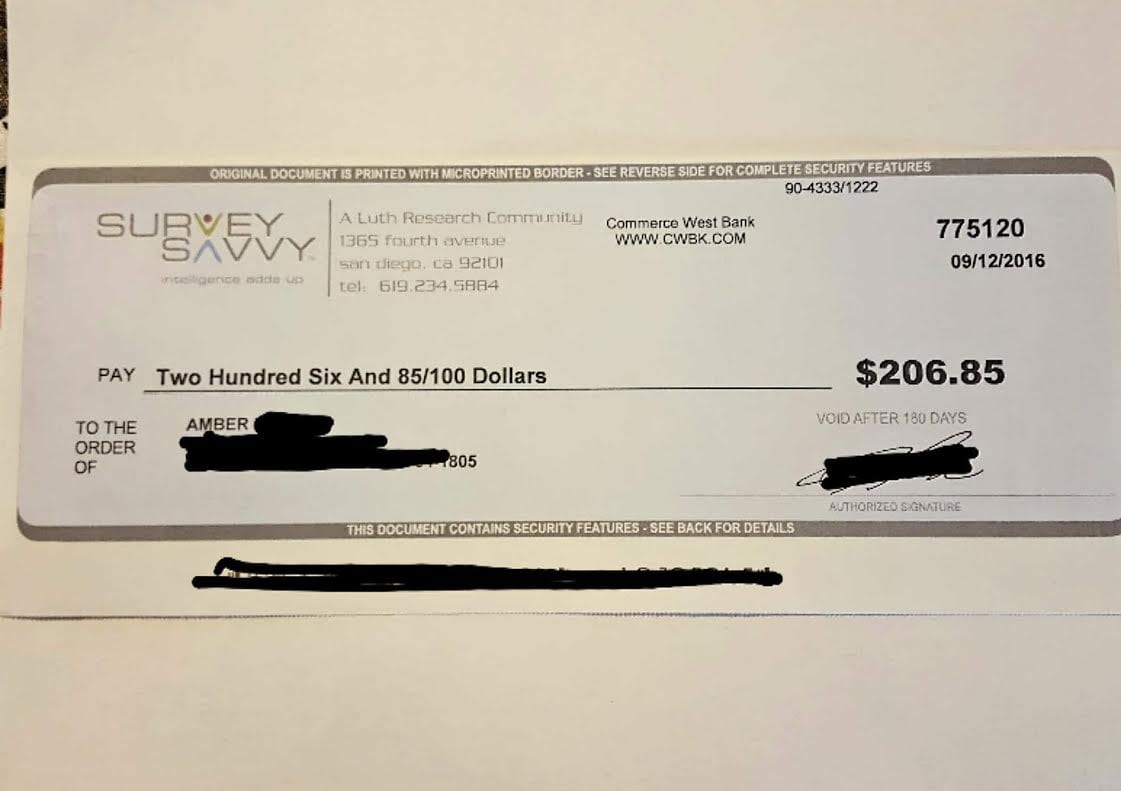

My latest check from SurveySavvy!

Put Credit to Work For You

If you knew me in college, you would have never thought I’d be someone you’d want to take financial advice from. When I turned 18 and was able to sign up for credit cards – WATCH OUT!

I remember sitting in my dorm room one night with a friend of mine and we were talking about money; she asked how I could sleep at night, knowing I had SO much credit card debt hanging over my head. I shrugged it off at the time, figuring I’d be in debt forever, have terrible credit, and who cares, right? At least I got that sweet PS2 so we could play DDR! (#collegelife amiright?)

In the years since then, I have paid for that silly gaming system many, many times over. Fortunately I’m happy to say I’m in a good place now with my credit and let me tell you – having good credit makes a world of difference in so many ways, especially when it comes to making credit work FOR you instead of AGAINST you.

Provided you’re like me now and not like 18 year old me, having a credit card can be a great thing. Personally, I have a Discover IT card because I’ll get DOUBLE all the cash back I earn in the first year but I definitely encourage you to shop around and find a card that best suits your needs. If you’re a hardcore Amazon shopper like I am, the Amazon.com Rewards Visa Card might be a better option for you (both offer a $50 sign-up bonus if you sign up via my referral link!)

Once you’ve got a great card that provides cash back, charge every bill that you can and then pay the card off IMMEDIATELY.

Do NOT adjust your budget. NO passing go. DON’T CHARGE ANYTHING YOU CANNOT PAY OFF THAT SAME MONTH!

Please.

Provided you use your card wisely, you’ll see a great amount of money back in your pocket.

Most cards are 1-2% back on everything, and then somewhere between 3% and 5% back on random specific things, like gas or groceries. Make sure it’s unlimited to some respect, even if it’s just the 1% back that’s unlimited.

Let’s say you have an Amazon.com Rewards Visa Card and you use it each month to pay for the following bills and purchases:

- Pet food/supplies, diapers, toilet paper, dry groceries – all Amazon purchases: $200

- Gas/Transportation: $100

- Trash Collection: $20

- Electric: $100

- Groceries in-store: $400

- Car insurance: $70

- TV (hopefully just Netflix/Hulu and not cable!): $15

Provided these are all in your budget as they should be, you will earn nearly $20 on expenses you had to pay anyway! So in this example, you’re basically getting trash service for FREE this month!

Depending on how you use it, you could be looking at hundreds of dollars back in your pocket for the year!

AND if you use it in conjunction with online shopping discount relays like Rakuten (formerly known as Ebates!), you can earn even MORE money back.

All told, you might end up with as much as 10% or more back on expenses you would have had to pay anyway.

Between cycling balances on my card and cashback from purchases made through Rakuten, I have earned about $400 so far this year, which then went directly to paying down debt.

Insiders Tip with a rebate site like Rakuten : Use it whenever you can! Many stores now offer in-store pick-up. Save yourself time and money by shopping through Rakuten for your purchases as often as possible. This will also help eliminate impulse spending if you go nowhere in the store but the service counter. (Check out how I’ve earned thousands from Ebates!)

How to get started…

Go through your budget and highlight in yellow everything you can pay for using a cashback rewards card. Calculate what you would earn back in a month if you used a card to pay for said expenses.

Then have an honest conversation with yourself about whether or not you can limit yourself to ONLY using your credit card for things already in your budget. If you can, then I highly encourage you to apply for one (as I mentioned, I like Discover or Amazon, but again – find one that works for YOU!)

If you have any doubt about using your card wisely, please don’t do it. Don’t put yourself in a situation that might lead to more debt instead of less.

And if you’re already using a cashback card, I do hope you’re using what you earn to pay down other debts and not to pay down your card’s balance.

Identify Why You Buy

Why do we take such great pleasure in buying things? Why does having “more” bring so many such comfort?

Maybe it provides a primal level of mental security, knowing you won’t go without. Or maybe, for some, it’s more of an ego-related feeling – “I’m wonderful and people will know that when they see I have these wonderful things!”

Perhaps it’s because you had nothing growing up and having “more” means staying away from those icky feelings from the past.

Here are some questions to help you pinpoint why you buy:

- Do you feel the need to “keep up with the Joneses”?

- Does your brand loyalty hurt your budget?

- Are you distracting yourself from inner dissatisfaction with new, shiny play things?

- Do you think brand name guarantees high quality?

- Are you addicted to luxury?

If you cannot identify “why you buy” then you will be unable to say “no” when the desire for more arises. By allowing yourself to constantly want, want, want, you are forcing yourself out of the present and living for what might be, for what you might acquire.

That’s not to say you shouldn’t live for the future. As you know, I’m all about developing long-term plans in order to kick debt to curb. However, you should focus on what will be, not what could be.

As is the case with budgeting your life overall, a long view of your purchases can help with this – a new shirt at full price might be $50 now, but that same $50 taken off of a credit card balance with 22% interest can end up being $60 or more.

Being able to view a purchase in terms of how much it will cost later on versus the immediate need to fulfill a desire will help immensely in avoiding impulse purchases. Like the adage “nothing tastes as good as being skinny feels,” no unnecessary purchase can bring you the peace of mind and reduce your stress like obtaining financial freedom.

Likewise, living in the past isn’t always a bad thing either. Think about where you were a couple years ago and what your household income was. Now think about what your expenses were. Are you spending more because you make more?

If you are in debt, you should not be upping your lifestyle to fit your current salary!

I know so many people who made $40,000/year, got a raise or better job, and instead of putting that additional income towards debt, they have now somehow incurred $10,000 more in expenses (often without realizing it!)

So how do you break these habits and learn to be happy with less?

Well, one of my favorite things to do is to keep a gratitude journal. I recommend against notebooks, simply because the covers are often flimsy, and you want to be able to carry this around with you. Any time you’re feeling down or you’re tempted by an extravagant purchase, pull out your journal and write down five things you’re grateful for.

Doing this will make you happier overall. I guarantee it.

Another thing to help you on your road to satisfaction with less is to consider where less already makes you happy.

For example, less clutter can equal MORE money and that almost certainly helps improve your mood, no? From the humble beginnings of trying to clear out stuff when we moved a couple years ago, to now where I almost constantly have stuff up on Facebook garage sale/resale groups, I’m averaging around $500 per garage sale and nearly $100/month on Facebook. Since November 2015 alone, I’ve made nearly $750 from selling things we no longer need (and this includes kids clothes that I actually got for FREE!)

I recently read a great book called The Brain That Changes Itself and one part that really stuck with me was that the more you practice saying no, the easier it’ll become.

How to get started:

Practice saying NO. Not just to others, but to yourself. Not only will this go a long way in helping your financial state, but it’ll actually re-wire your brain and lead to a healthier, better life overall. How cool is that?

(Re)Define Your Budget!

It’s not enough to make broad goals like “I want to lose weight” or “I will be financially independent”. It’s great to use these as a part of your affirmations but as goals? No.

You must be specific, B-E specific!

You should create and define clear goals that will build towards that momentous success of living a better life on a budget.

Instead of “I will stop using my credit card and pay it off!” Come up with a plan to pay off that card in X number of months. Figure out exactly what’s causing you to use the card now and how you’re going to stop those behaviors.

If physically cutting up the card gives you anxiety, consider freezing it – literally. Put it in a bowl of water and stick it in the freezer. It won’t eliminate your access to it but it’ll certainly give you time to think about whether or not you really need it to make that purchase.

Once you’ve set your goals, take a look at your budget and figure out your plan of action. I recommend starting by immediately cutting your budget by 5%.

Impossible, you say?

When I started this journey in January, I was able to take our $2,500/month income and trim it up by an additional 8%. I too thought it impossible at first until I took the time to develop an action plan.

After evaluating your financial budget, take an honest look at how you’re spending your time. Just as small purchases add up – a $3 cup of coffee doesn’t seem so bad…until you realize a canister of coffee at home would only cost you $10 for at least two weeks of coffee… – so do the “time sucks.”

Sure, maybe you only spend an hour watching TV each night but what if in that hour you could be earning $20? That’s over $7,000/year (nearly $9,000 if that $7k is on an unpaid credit card with 22% APR!)

I’m not suggesting you use every minute of every day to work towards paying down your debt. You must take the time for self-care in more than one way and if that means watching a bit of TV, then go for it! The important part is making sure you’re not wasting hours now that you may not have later.

So there you have it!

In two months, I was able to pay down my debt by over $10,000 by:

- Paying based on interest rates

- Putting my tax return to use

- Developing additional income streams

- Making credit work for me instead of against me

- Identifying and breaking the habits that lead to wanting more

- Redefining the way I budget my life

Our debt, while still quite high, now looks like this:

- Lowes Credit Card: $0

- Furniture Row Credit Card: $0

- Student Loans: 138,116.82

- House: $42,800

- Car: $17,816

Total: $198,303.82

Difference of $10,588.67

I can’t say this has been an easy road, nor will it get any easier any time soon, but there is not a doubt in my mind that this is the best path towards a better, healthier, happier life.

I know this is a long post (and probably a bit overwhelming) but if you take it one step at a time, you too can pay down a significant amount of debt in a short amount of time!

This is a super helpful and inspirational piece, Amber.

This is SUCH an awesome post- at some point, we all struggle with debt, and this definitely helps us see the light at the end of the tunnel- THANK YOU!

Amber…amazing insight on debt management! Thank you so much!